UK Gambling Commission Data Uncovers Mixed Trends: Online GGY Dips 2% to £1.5 Billion in Q3 2025-26 While Bets and Spins Climb

Operators across Great Britain have handed over fresh data to the UK Gambling Commission, painting a picture of gambling activity that spans from March 2020 right through to December 2025; published in February 2026, these figures dropped just as the industry geared up for what many observers call a pivotal spring season in March 2026, revealing not just quarterly snapshots but long-term shifts shaped by regulations and player habits.

Overview of the Latest Operator-Sourced Statistics

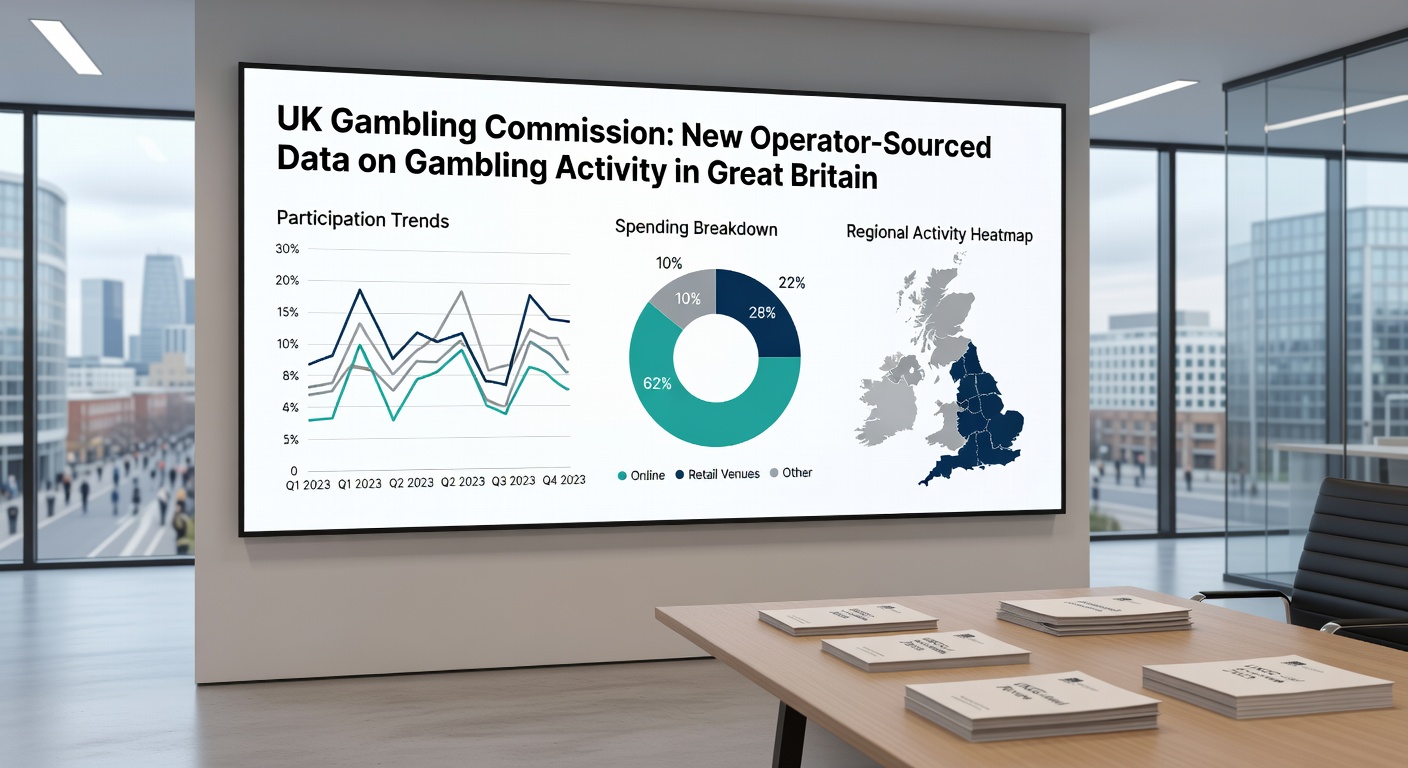

Data covering the full period shows mixed trends emerging especially in the most recent quarter, Q3 of the 2025-26 financial year, where online Gross Gambling Yield—or GGY, the net profit from gambling after payouts—edged down 2% to £1.5 billion even as total bets and spins surged 6% to a hefty 27.4 billion; this contrast underscores how player engagement keeps climbing, yet revenue per activity dips, a pattern that experts tracking the sector have noted ties directly to affordability checks and stake restrictions rolling out over recent years.

What's interesting here lies in the broader timeline starting back in March 2020, when lockdowns first reshaped habits toward online platforms; fast forward through peaks during major events and regulatory tweaks, and the data captures everything up to December 2025, offering operators and regulators alike a benchmark as they navigate early 2026 uncertainties.

And while overall online GGY holds steady in some segments, the quarterly decline signals where the rubber meets the road for businesses balancing volume against margins; figures reveal this 2% drop happened against a backdrop of heightened activity, with spins and bets not just ticking up but jumping notably, hinting at more frequent, lower-value wagers becoming the norm.

Real Event Betting Takes a Hit: 18% GGY Plunge to £530 Million

Real event betting, that staple covering sports and races where outcomes hinge on live action, saw its GGY tumble 18% to £530 million in Q3 2025-26; observers point to seasonal lulls post-summer leagues or shifts in how punters spread their play, but the data ties this drop to broader participation trends where total sessions might rise without proportional spending boosts.

Take one segment of the data stretching back to 2020: early pandemic years showed spikes in event betting as fans turned to virtual thrills, yet by late 2025, with stake limits and safer gambling tools in place, yields compressed; people who've analyzed these patterns often discover that while bet volumes hold firm, the average stake per bet shrinks, leading to that sharp revenue contraction.

But here's the thing—total activity metrics climbed alongside, suggesting players chase more events or diversify, spreading thinner across football, horse racing, and beyond; this 18% dip, stark against the 6% overall bets rise, highlights how real-world unpredictability in events doesn't always translate to windfalls for operators anymore.

Slots Buck the Trend: 10% GGY Rise to £788 Million Amid Stake Limit Effects

Slots tell a different story altogether, with GGY climbing 10% to £788 million in the same quarter and spins increasing 7%, a rebound that data attributes squarely to the new online stake limits of £5 for ages 25-plus and £2 for under-25s introduced in 2025; these caps, meant to curb high-rolling risks, seem to have spurred more spins at lower stakes, boosting volume enough to lift overall yields.

Figures from the Gambling business data report detail how this played out: pre-limit periods showed heavier concentration on big bets, but post-2025, spins distributed more evenly, turning slots into a high-frequency haven; researchers examining operator returns note that this 10% uptick, paired with the 7% spin growth, reflects adaptation—players spin more often within bounds, and operators see margins hold via sheer numbers.

Now consider the full arc from March 2020: slots endured volatility through economic squeezes and regulatory previews, yet ended 2025 stronger, a segment where limits didn't just contain losses but amplified engagement; it's noteworthy that while real events faltered, slots' resilience points to digital games thriving under constraints, with 27.4 billion total spins underscoring the shift.

Long-Term Patterns from March 2020 to December 2025

Zooming out to the entire dataset, trends weave a tapestry of growth tempered by controls; online GGY across quarters fluctuated—up during 2021-22 booms tied to eased restrictions, steadying later as affordability measures bit—but Q3 2025-26's 2% dip marks a pivot, coinciding with stake implementations that reshaped slots while pressuring events.

Total bets hitting 27.4 billion in that quarter alone dwarf earlier figures, say from Q1 2020's lockdown lows, showing sustained online migration; data indicates sessions per player lengthened slightly, yet average GGY per session compressed, a dynamic those who've studied operator filings recognize as the hallmark of regulated maturity.

Yet slots stand out across years: their 10% quarterly gain builds on prior resilience, with spins up consistently post-limits; real event betting, conversely, shows cyclical dips—18% now echoing softer winters past—while overall yield's 2% slide masks segment wins and losses balancing precariously.

One case from the data highlights this: mid-2025 previews of limits correlated with preemptive spin surges, smoothing the transition; by December, the ecosystem stabilized, setting the stage for March 2026 analyses where operators watch if these patterns hold through spring sports.

Key Metrics Breakdown and Regulatory Context

Delving deeper, the report breaks out participation alongside yields: 6% bets/spins growth to 27.4 billion means billions more interactions, from casual slots flurries to event accumulators; GGY's £1.5 billion online total, down 2%, splits into slots' £788 million gain offsetting events' £530 million loss, a zero-sum vibe where volume compensates.

Stake limits' fingerprints appear everywhere—£5/£2 caps on slots directly fueled that 7% spin jump, as players adjust downward without quitting; experts parsing the numbers observe how this echoes prior casino duty hikes, where activity rebounded via frequency over fortune.

And across the 2020-2025 span, monthly data points reveal inflection moments: 2022 World Cup peaks in events, 2024 pre-limit caution, 2025 adaptation surges; Q3's mix—yield dip but activity boom—signals where that's headed, especially with February 2026's release timing bets on 2026 fiscal health.

- Online GGY: -2% to £1.5 billion (Q3 2025-26)

- Total bets/spins: +6% to 27.4 billion

- Real event GGY: -18% to £530 million

- Slots GGY: +10% to £788 million; spins +7%

Such granularity helps stakeholders gauge impacts, from operator profitability to player safeguards, all operator-sourced for reliability.

Implications for the Road Ahead in 2026

As March 2026 unfolds with fresh events on horizons, these figures serve as a compass; the 2% GGY softening warns of margin pressures if volumes don't sustain, while slots' strength suggests digital resilience under rules—real events must innovate to claw back.

Data shows limits working as intended, curbing extremes yet preserving play; operators who've leaned into data-driven tweaks often find session metrics stabilize, a lesson from 2025's playbook.

Turns out, the full 2020-2025 view confirms evolution: from pandemic piv